Speed vs. Substance: Singapore’s Wealth Strategy Pivot 🇸🇬

The paperwork is getting faster. But can the rules keep up with modern portfolios? A deep dive into the SFO “tweak” that matters.

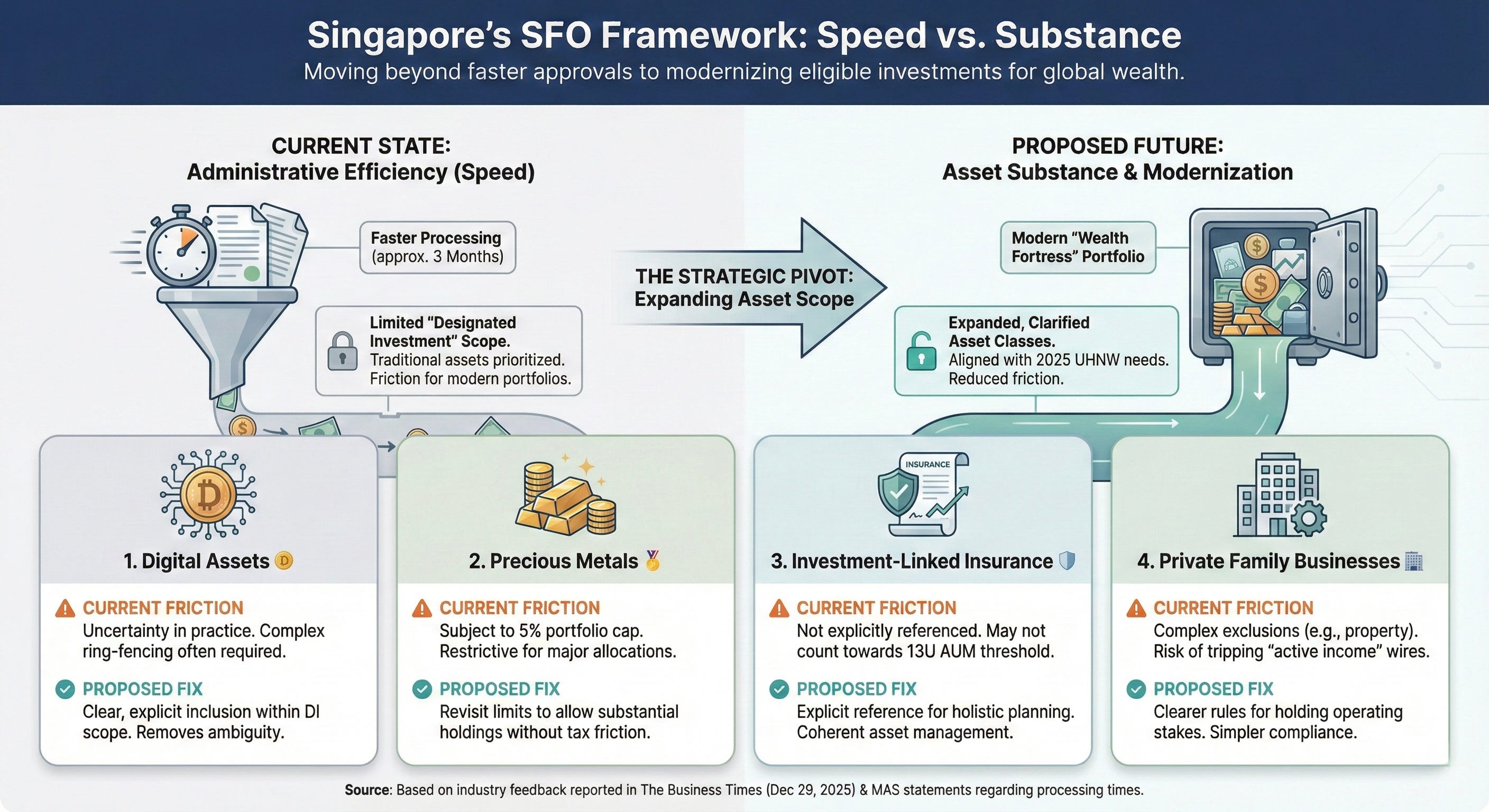

If you have been watching the wealth management space in Singapore, the noise has mostly been about bottlenecks. For the past year, the backlog for tax incentive applications was the industry’s collective migraine.

But the Monetary Authority of Singapore (MAS) has quietly moved the needle here. Deputy Chairman Chee Hong Tat recently confirmed that processing times have dropped from nearly a year to around three months. The “speed” problem is largely being solved.

So when The Business Times reported on Dec 29, 2025, that industry players are lobbying for further tweaks, the story wasn’t about administrative efficiency.

It was about asset scope.

For the first time in a while, there is serious momentum behind expanding the “Designated Investment” (DI) list. For modern Ultra-High-Net-Worth (UHNW) families, this shift from “how fast can I apply?” to “what can I actually invest in?” is the strategic pivot that matters.

Let’s dive in.

The “Designated” Definition

To understand the debate, we have to look at the engine of Singapore’s wealth hub: the 13O and 13U tax incentive schemes.

In plain English, if you meet the conditions (like minimum spend and fund size), your fund vehicle gets a tax exemption on “specified income.” But there is a catch. That income must come from “Designated Investments” (DI).

This isn’t a vague concept. It is a strictly defined legal list. While the DI list is broad and covers most standard financial instruments (shares, bonds, derivatives), it has historically drawn a hard line around certain asset classes.

The industry is now arguing that this list needs an update to reflect 2025 portfolios. Here are the gaps and what might change.

1. Digital Assets 🪙

The Status Quo: While the DI list is comprehensive for traditional finance, the framework does not clearly and explicitly accommodate the full spectrum of digital assets today.

The Friction: As a result, for DI eligibility purposes, whether income from these assets qualifies under the incentive can be uncertain in practice.

The Fix: Industry observers are lobbying for digital assets to be clearly brought within the scope of Designated Investments. This would remove the need for complex structuring just to ring-fence crypto assets.

2. Precious Metals 🥇

The Status Quo: There is a misconception that gold doesn’t count at all. That’s not quite right. Since February 2022, “Investment Precious Metals” (IPM) has been included in the DI list.

The Catch: This inclusion is subject to a cap of 5% of the total investment portfolio.

The Goal: For families using physical bullion as a major inflation hedge, that cap is restrictive. Some in the industry may push to revisit these limits to allow for more substantial allocations to physical commodities without tax friction.

3. Investment-Linked Insurance 🛡️

The Status Quo: Wealthy families frequently use Universal Life (UL) or Private Placement Life Insurance (PPLI) for liquidity and succession planning. However, insurance policies are not explicitly referenced in the DI framework, and industry commentators have proposed adding insurance products to reduce structuring friction.

The Friction: This limits how cleanly SFOs can house insurance wrappers under the same incentive framework. Crucially, if a large slice of wealth sits in these structures, it may not contribute toward the S$50 million in Designated Investments threshold commonly associated with the 13U scheme.

The Ask: Clearer inclusion. This would allow families to manage protection and investment assets more coherently under one roof.

4. Private Family Businesses 🏢

The Status Quo: SFOs often hold stakes in private operating companies. While shares in private companies generally can count as Designated Investments, the devil is in the details.

The Friction: The challenge often revolves around distinguishing “passive investment income” from “active operating business income” and navigating well-known exclusions (notably those related to certain property-holding/trading profiles).

The Goal: Clearer rules would help families retain their operating business stakes through the SFO structure without inadvertently triggering “active income” rules.

The Verdict: From Hub to Fortress

If MAS executes on these suggestions, it signals a shift from Singapore being a “Traditional Wealth Hub” to a “Modern Wealth Fortress.”

Competitors like Hong Kong and Dubai are aggressively courting crypto wealth and offering flexible structures. By modernising the definition of “investments” (clearing up the uncertainty around crypto, revisiting limits on gold, and formalising insurance), Singapore ensures its regulatory framework matches the actual portfolios of the families it wants to attract.

What’s next? If these changes go through, the implications for service providers, from insurance brokers to crypto custodians, will be massive. I’ll break down the specific business opportunities in the industry in my next post.

Thanks for reading. If you found this deep dive into Singapore’s regulatory landscape helpful, subscribe for more updates.

If you found value in this article, please hold down the like ❤️ button or consider buying me a coffee ☕️ to fuel the next one!