The 2026 CPF Shift: 6 Changes That Will Hit Your Wallet (And How to Prepare)

From salary ceilings to senior rates, here is the “adulting” manual you didn’t ask for but definitely need.

Let’s be honest: “CPF policy update” is not a phrase that usually sparks joy. It usually sparks a frantic mental calculation of “Wait, does this mean I have less spending money next month?”

If you’ve been feeling like the goalposts for financial planning keep moving, you aren’t imagining it. The system is evolving to cope with a reality we can’t ignore: we are living longer, medical costs are rising, and the traditional “9-to-5” career is disappearing.

Come January 1, 2026, Singapore is rolling out six major structural changes to the CPF system. Some will pinch your monthly cash flow. Others offer “free money” from the government—if you know how to unlock it.

Whether you are a high-income earner, a senior executive, or a gig worker, here is the no-nonsense breakdown of what’s changing—and the exact moves you need to take now.

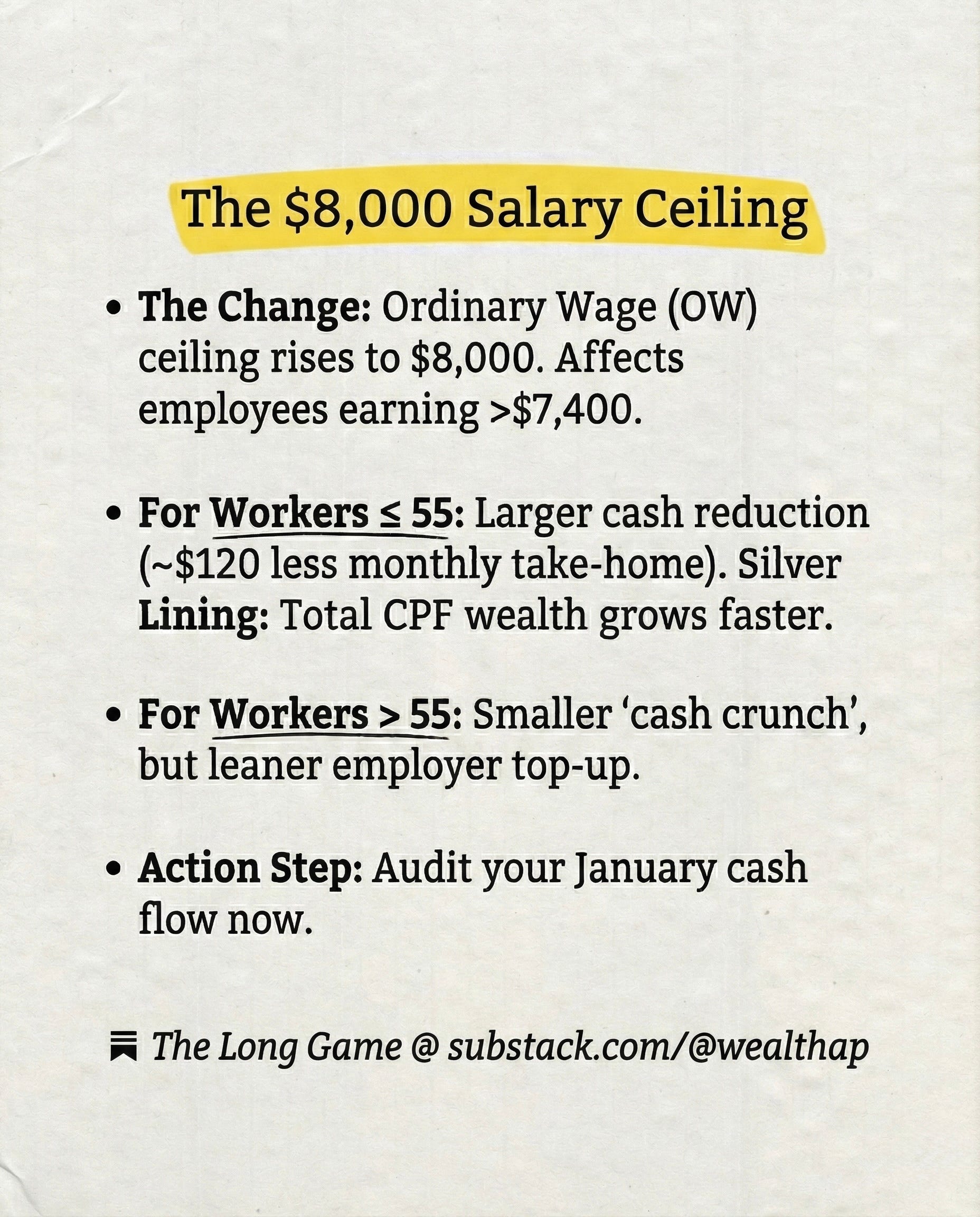

1. The Final “Ouch” for High Earners: $8,000 Salary Ceiling

The Ordinary Wage (OW) ceiling hits its final target, rising from $7,400 to $8,000 on Jan 1, 2026. This affects all employees earning above $7,400, but the impact on your wallet varies significantly by age.

For Workers Aged 55 and Below: This group faces the largest monthly cash reduction because their contribution rate is the highest (20%). You will see $120 less in your monthly take-home pay (20% of the additional $600).

The Silver Lining: Your employer matches this with an extra $102 (17% of $600). It feels like a cut, but your total CPF wealth (OA + SA + MA) actually grows faster.

For Senior Workers (Above 55): You are also affected by the ceiling rise, but your “cash crunch” from this specific change is smaller because your employee contribution rates are lower than those of your younger colleagues.

The Trade-off: While the deduction from your take-home pay is lower, the employer top-up you receive on that extra portion is also leaner compared to younger workers.

Action Step: Audit your January cash flow now. If your budget is tight, factor in this reduction immediately so your first 2026 payslip doesn’t come as a shock.

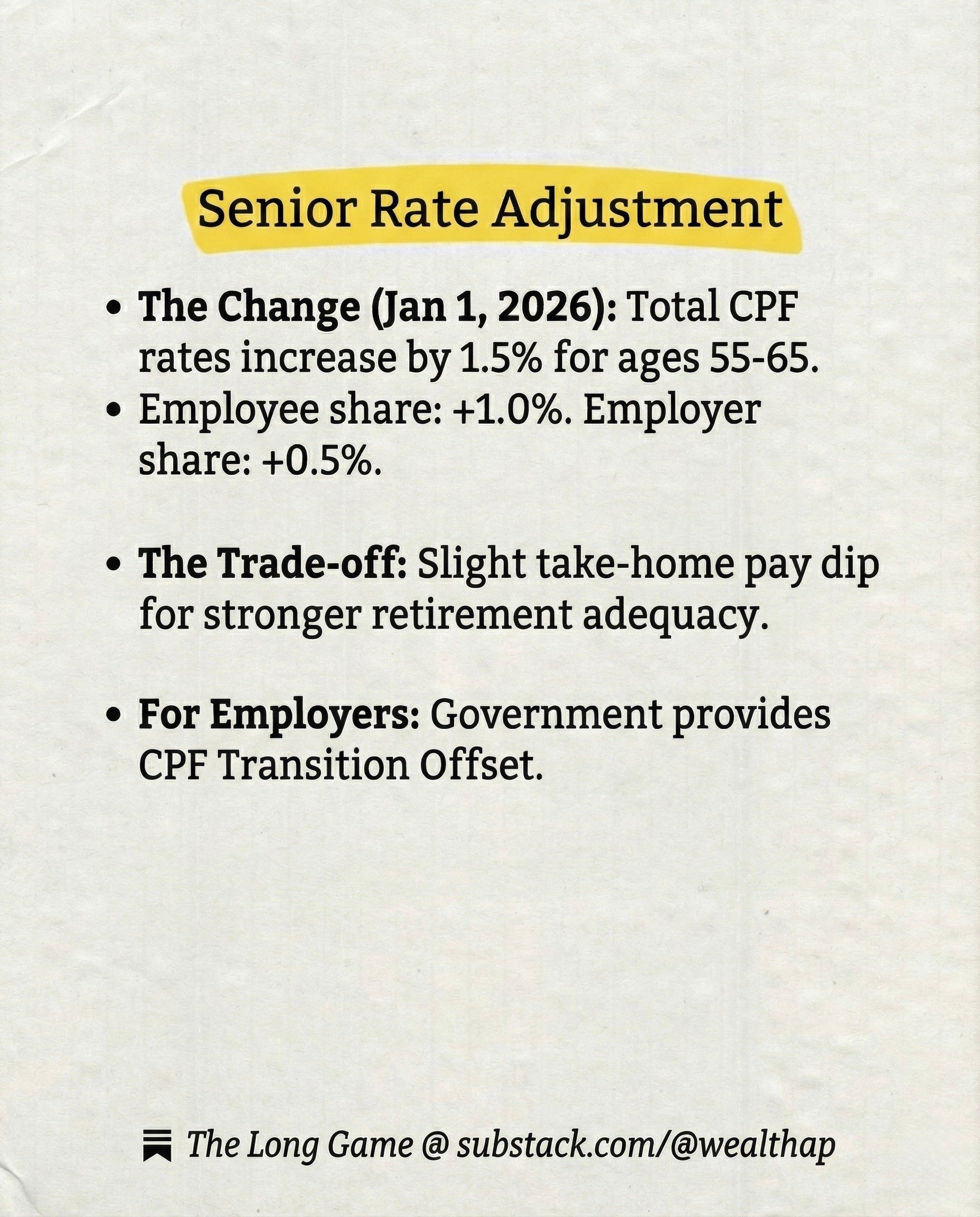

2. The Senior Rate Adjustment (Ages 55 to 65)

Beyond the higher Ordinary Wage (OW) ceiling, senior workers will also see a scheduled CPF contribution rate adjustment in 2026 as part of Singapore’s broader effort to strengthen retirement adequacy.

The Change (Effective 1 January 2026): For employees aged above 55 to 65, total CPF contribution rates will increase by 1.5 percentage points compared to 2025, as announced by the Central Provident Fund Board.

Employee share: +1.0%

Employer share: +0.5%

This increase applies to both age bands:

Above 55 to 60

Above 60 to 65

Note: Employees aged 55 and below, as well as those above 65, will see no change to their contribution rates.

One-Line Comparison vs 2025: In 2026, senior workers aged 55–65 will contribute 1.5 percentage points more of their monthly wages to CPF than in 2025, with one-third borne by employers and two-thirds by employees.

The Impact on You: Your monthly take-home pay will dip slightly due to the higher employee contribution rate. At the same time, more CPF savings are accumulated, primarily flowing into your Retirement Account (RA) (since the Special Account is closed for those aged 55+), which strengthens your ability to:

Fully fund your Retirement Account (RA) at age 55, and

Reach the Full Retirement Sum (FRS) earlier or with less reliance on top-ups.

In short, this is a cash-flow trade-off for stronger retirement adequacy.

The Impact on Employers: To ease cost pressures, the government will continue the CPF Transition Offset in 2026, covering 50% of the employer’s additional CPF contribution arising from this rate increase. This helps moderate hiring costs while supporting the employment of experienced senior workers.

Action Step: Log in to your CPF account and review your projections under tools such as “Plan My Monthly Payouts.” With both the higher OW ceiling and the senior rate adjustment in play, your CPF balances — and progress toward the FRS — may be stronger than expected.

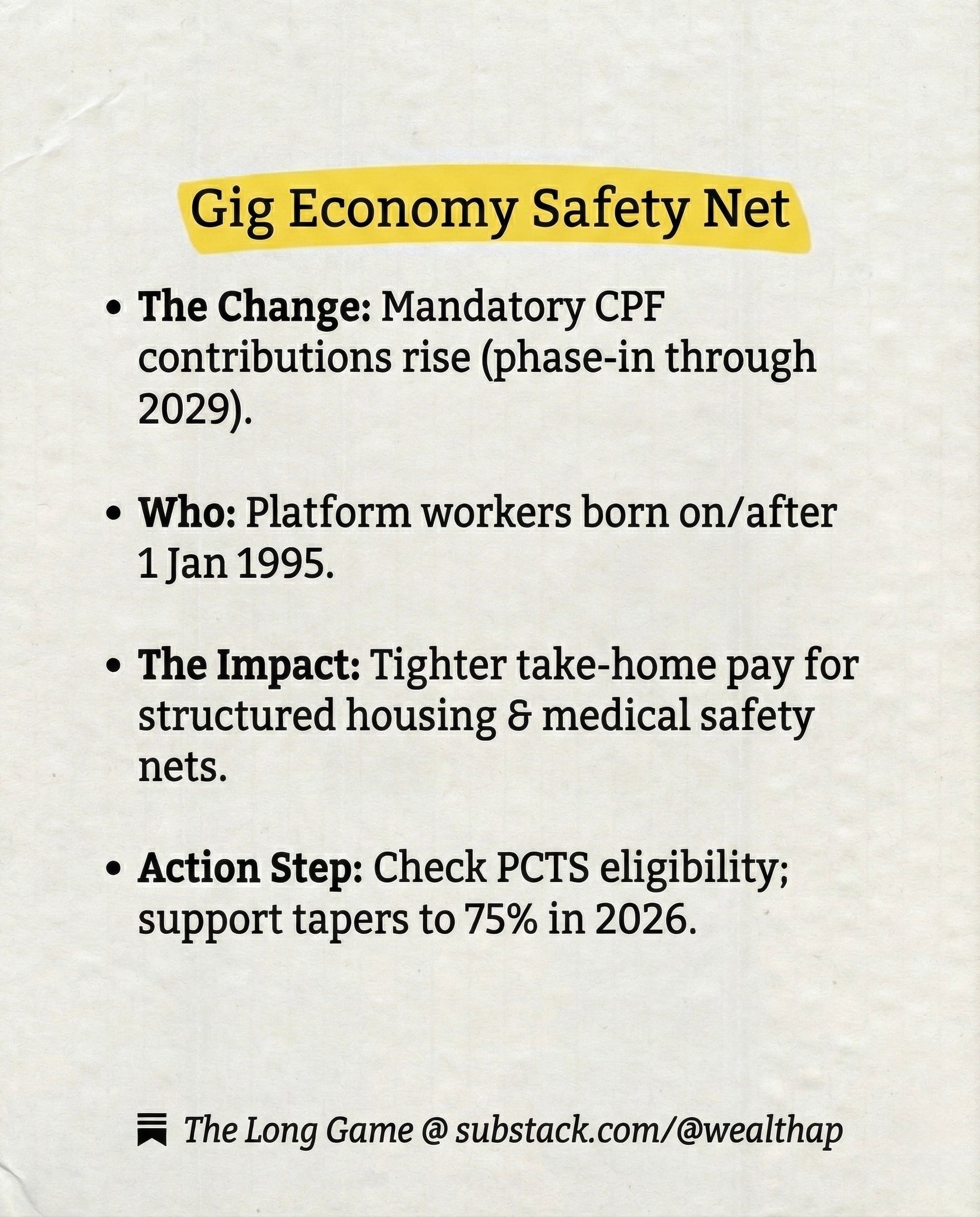

3. The Gig Economy Safety Net

The “Wild West” era of the gig economy is officially closing. Mandatory CPF contributions for platform workers will increase again in 2026, as part of a five-year phase-in through 2029 to strengthen parity with standard employee protections.

Who is affected: Delivery partners and private-hire drivers born on or after 1 January 1995, as well as older platform workers who have opted in.

The impact: Take-home pay may feel tighter as CPF contribution rates continue to rise. In return, platform workers gain a more structured footing in housing and medical safety nets without relying on a traditional employer.

Action step: Note that the Platform Worker CPF Transition Support (PCTS) — which subsidises part of the incremental increase in your CPF contributions — tapers from 100% support in 2025 to 75% in 2026, subject to income eligibility. Check whether you remain eligible to see how much of the increase continues to be subsidised.

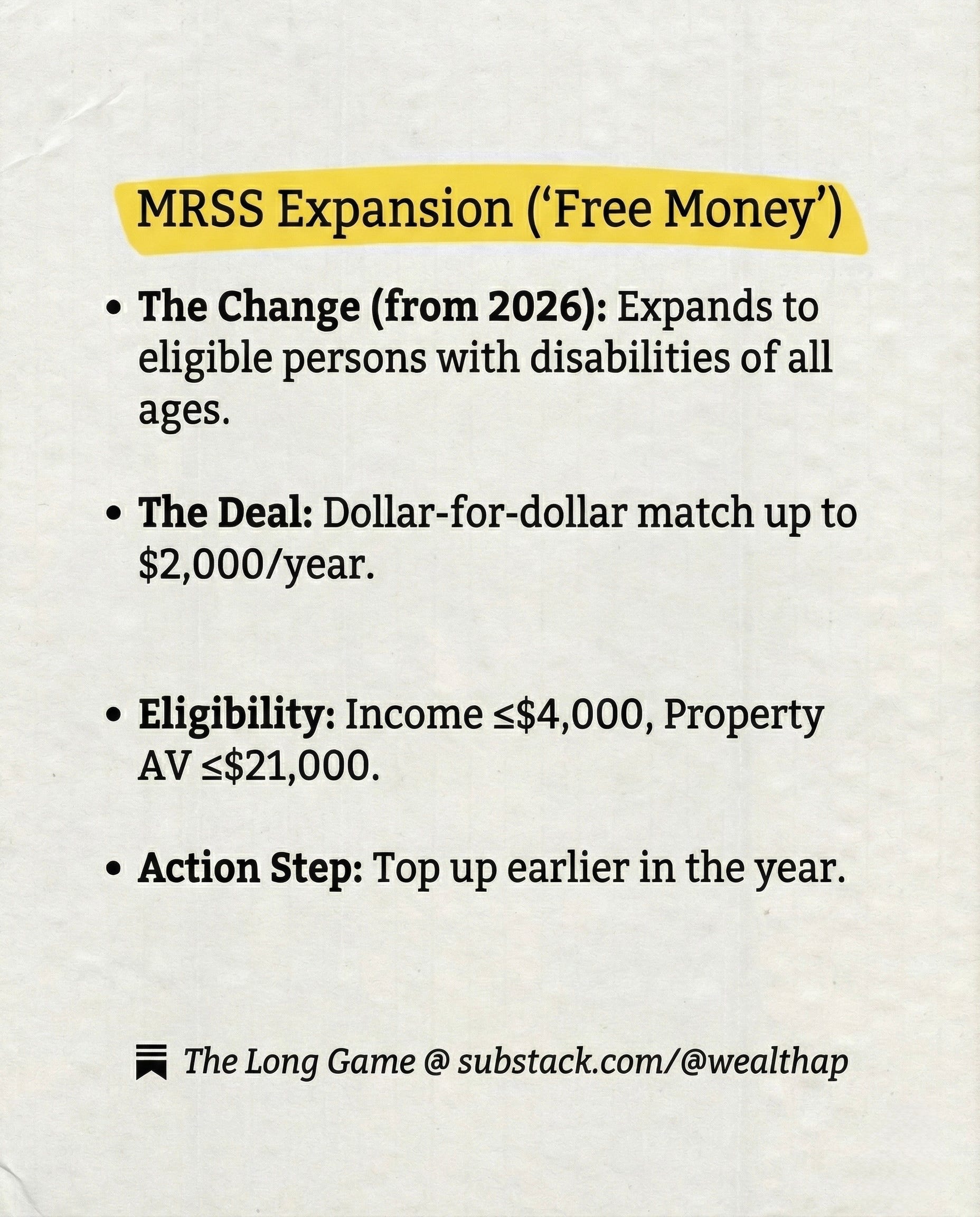

4. The “Free Money”: MRSS Expansion

The Matched Retirement Savings Scheme (MRSS) is becoming more inclusive. The annual government matching cap has already been doubled to $2,000, and from 2026 onwards, the scheme expands to cover eligible persons with disabilities of all ages, removing the previous age floor.

The Deal: If you qualify — monthly income of $4,000 or less and property annual value of $21,000 or less — the government will match your cash top-ups dollar-for-dollar, up to $2,000 per year. Top-ups go to the RA (age 55 and above) or SA (below 55), delivering a guaranteed government match that no market investment can replicate.

Action Step: Do not wait until year-end. Making your top-up earlier in the year allows CPF interest to work in your favour for longer.

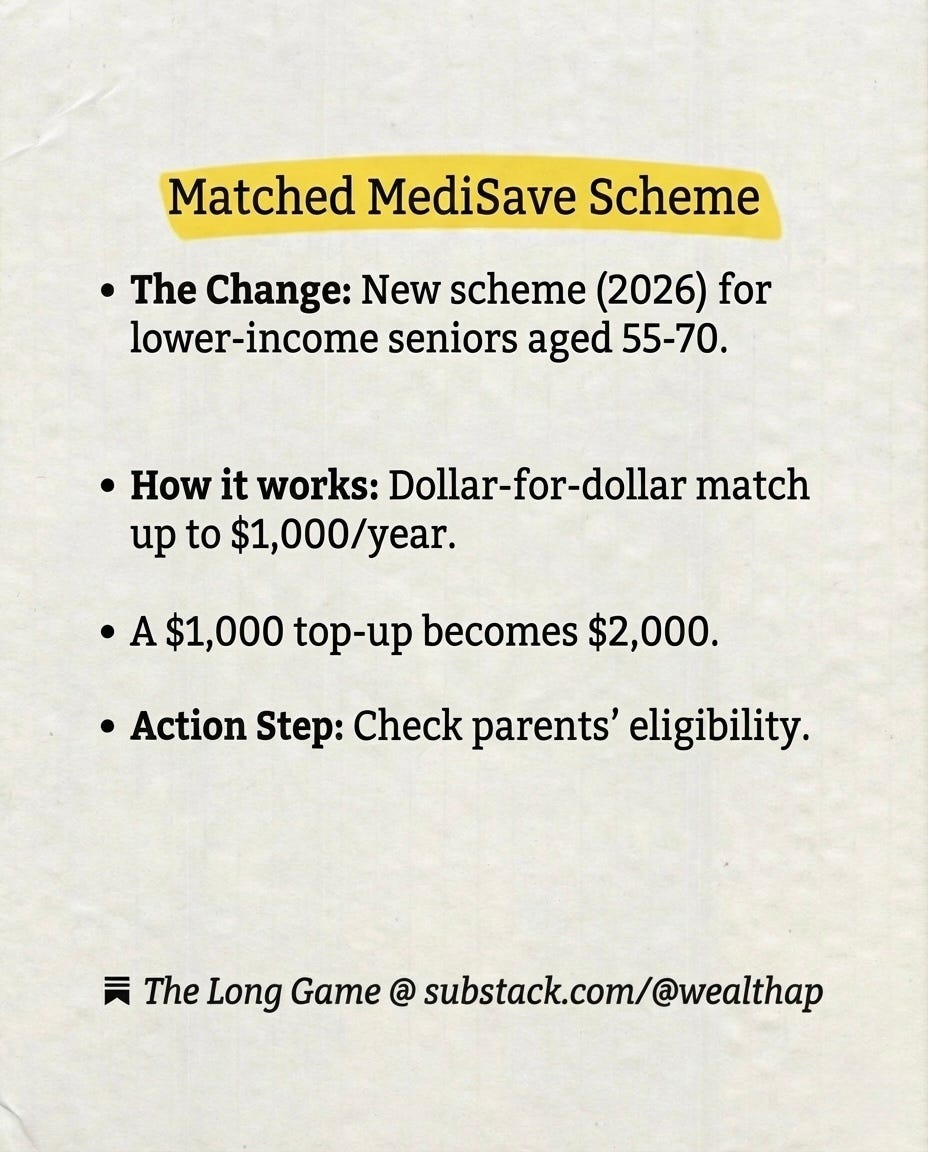

5. Healthcare Support: The Matched MediSave Scheme

Starting in 2026, a new Matched MediSave Scheme will be introduced to help lower-income Singaporeans aged 55 to 70 strengthen their healthcare savings.

Who is it for: Eligible seniors aged 55 to 70 with lower MediSave balances, subject to income and property criteria.

How it works: The government will match every dollar of cash top-up to your MediSave Account, up to $1,000 per year, effectively doubling the impact of your contribution.

Action Step: Check your parents’ eligibility. If they qualify, a $1,000 cash top-up becomes $2,000 in MediSave, making this one of the most efficient ways to bolster your family’s healthcare buffer against rising medical costs.

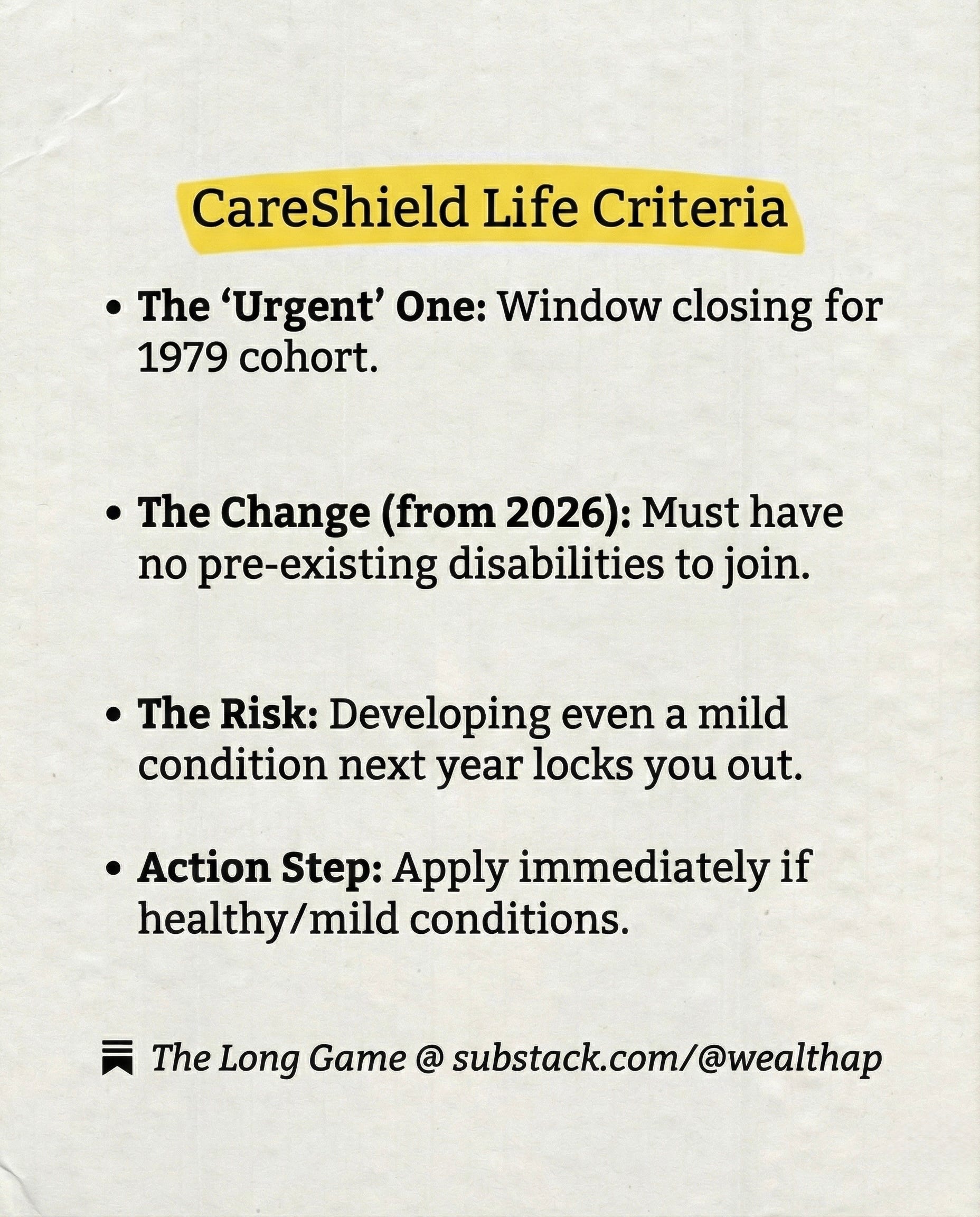

6. The “Urgent” One: CareShield Life Criteria

This is the most time-sensitive update. For Singaporeans born in 1979 or earlier, the window to join CareShield Life (the national severe disability insurance) is easily closing.

The Change: From 2026 onwards, participation criteria will tighten significantly. You will only be able to join if you have no pre-existing disabilities (meaning you must be fully able-bodied). Currently, you can still join even with mild or moderate disabilities.

The Risk: If you have been procrastinating and you develop even a mild condition next year, you could be permanently locked out of the scheme.

Action Step: If you or your parents are in the 1979-or-earlier cohort and are currently healthy or have only mild conditions, apply immediately. Do not risk the underwriting changes coming in 2026.

Conclusion: It’s About the Long Game

These changes might feel like a flurry of administrative tweaks, but they tell a clear story: Self-reliance is becoming expensive, and state support is becoming more targeted.

The $8,000 ceiling forces high earners to save more. The MRSS and new MediSave schemes reward those who actively plan. The message is simple: You cannot just “drift” into retirement anymore.

Your Immediate Checklist:

Adjust your 2026 budget: Factor in the drop in disposable income if you earn >$7,400.

Apply for CareShield Life: Do it now if you (or your parents) are born before 1980.

Set a reminder for Jan 5, 2026: “Top up CPF for MRSS/MediSave matching.”

Future You will thank Present You for paying attention today.

Disclaimer: This article is for educational purposes and does not constitute financial advice. Policy details can change; always refer to the official CPF Board and MOH websites for the latest eligibility criteria.