The $325 Billion Warning: What Warren Buffett’s Final Moves Reveal About the Global Economy

The Oracle of Omaha is hoarding cash and dumping tech. Here is why the greatest investor in history is preparing for an unprecedented financial storm.

Welcome to The Long Game ♟️, a newsletter about long-term investing and money matters. If you’d like to support this, please subscribe.

The Long Game ♟️Perspective An occasional value investing series:

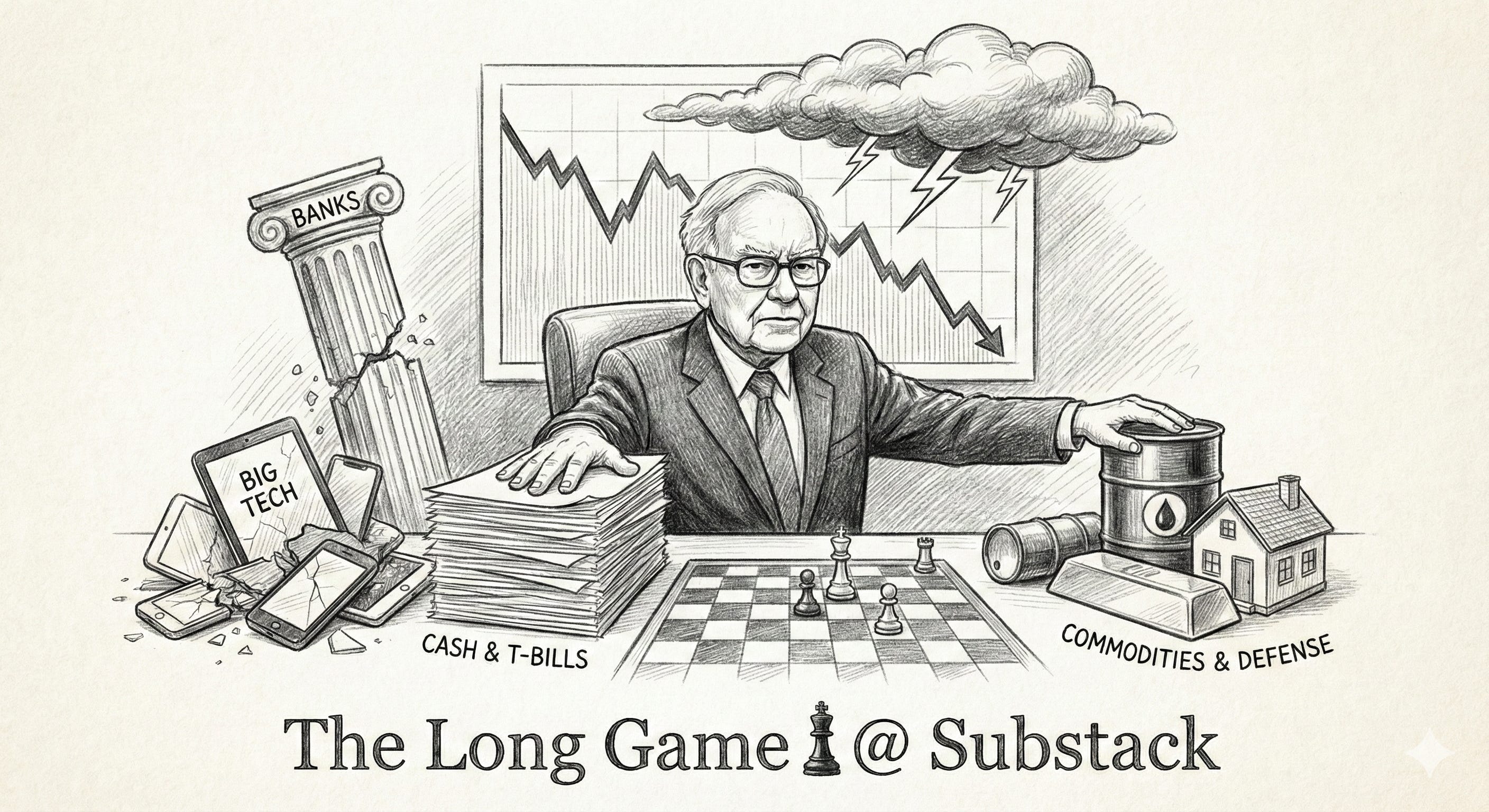

Warren Buffett has officially stepped down from his role as the Chief Executive Officer of Berkshire Hathaway. He handed the operational reins to Greg Abel on December 31, 2025, though he remains a looming presence behind the scenes as Chairman. His final quarter as the chief capital allocator of the world’s most famous conglomerate was nothing short of historic. But if you look closely at his latest SEC filings, the Oracle of Omaha is not taking a victory lap in the tech-driven bull market. Instead, he is sending a terrifying signal to every stock market bull in America.

While retail investors and hedge funds endlessly chase artificial intelligence hype, Buffett is systematically liquidating his exposure to the modern digital economy. He is rotating heavily out of financial assets and into defensive legacy businesses, hard commodities, and an unprecedented mountain of cash. By analysing his latest buying and selling patterns, a clear and highly provocative picture emerges. Buffett is bracing for a macroeconomic storm of historic proportions.

The Great Liquidation of Tech and Banks

To understand what Berkshire is building, we first have to look at what they are tearing down. In his final quarter as CEO, Buffett executed a series of aggressive sales across his most profitable positions.

He systematically slashed his single largest holding, Apple, reducing the massive position by half. At previous annual meetings, Buffett hinted that selling these highly appreciated shares was a strategic move driven by tax considerations. Berkshire was sitting on tens of billions of dollars in unrealised gains. Buffett believes that in the next ten years, corporate tax rates will inevitably rise to address the national deficit. By selling now, he locks in the current capital gains rates before the fiscal environment deteriorates.

But the selling went much deeper than just taking profits on Apple. Berkshire completely abandoned the prevailing Wall Street narrative by slashing its stake in Amazon by a staggering 77 per cent. Initially purchased in 2019 by one of his investment deputies, the Amazon stake saw decent returns of around 130 to 140 per cent, performing roughly in line with the broader S&P 500. However, the decision to dump the stock highlights a fascinating ideological split among the world’s super investors.

Currently, massive tech companies like Amazon and Meta are pouring billions into capital expenditures to build out their artificial intelligence infrastructure. Investors like Bill Ackman are happily buying Amazon. They argue that this heavy spending is a deliberate choice driven by massive, predictable customer demand for cloud computing. The market is actively punishing Amazon for this spending, pricing it at a 26.5 forward price-to-earnings ratio. Meanwhile, traditional retailers like Walmart trade at an exorbitant 43 forward PE despite growing at a fraction of Amazon’s speed. Ackman views Amazon as a bargain, but Buffett clearly disagrees. Berkshire prefers companies producing reliable free cash flow today over those burning cash for a theoretical technological advantage tomorrow.

Alongside big tech, Buffett has actively reduced his exposure to the financial sector. He shed nearly 9 per cent of his massive Bank of America position, while also trimming stakes in banks like Wells Fargo and US Bancorp over recent years. This is a broad-based, deliberate de-risking of the portfolio across multiple sectors.

The Five “Boring” Defensive Buys

While Buffett was busy selling tens of billions of dollars in tech and banking stocks, he deployed a highly targeted $3 billion into exactly five companies during the quarter. A separate report indicated a $4 billion purchase of Alphabet, suggesting his deputies might still see isolated value in search monopolies. However, Buffett’s direct legacy purchases paint a decidedly old-school, defensive picture.

The new purchases epitomise boring, reliable cash flow.

First, Berkshire added $900 million to its position in Chubb Limited, bringing the total stake to nearly $10.7 billion. Chubb is the largest publicly traded insurance company in the world. It boasts operations in over 50 countries, phenomenal management, and double-digit net income growth. Buffett has always utilised massive insurance float to power Berkshire’s investments, making Chubb a natural fit. The acquisition is deeply strategic. Chubb’s speciality commercial and personal property operations perfectly complement Berkshire’s existing massive Geico auto business and global reinsurance arm. With Chubb’s market cap sitting at $130 billion, some analysts speculate that Buffett might be running his old Burlington Northern playbook. He could be initiating a public stake with the eventual goal of buying the entire company outright.

Second, Berkshire aggressively added $1.3 billion to Chevron, elevating the oil giant to the fifth-largest holding in the portfolio at nearly $20 billion. Beyond its robust 4 per cent dividend yield, this acts as a brilliant geopolitical energy play. Recent US interventions regarding Venezuela’s oil reserves uniquely position Chevron to benefit. They were the only major American oil producer maintaining operations on the ground with a special license. They possess the infrastructure and the relationships to capitalise on shifting global oil dynamics.

Third, Buffett increased his stake in Domino’s Pizza by 12 per cent, pushing the holding to $1.4 billion. In the notoriously volatile and low-barrier fast food industry, Domino’s has carved out an exceptional moat. They dominate the global market share by offering irresistible consumer value, leveraging a highly addictive digital rewards program, and consistently delivering steady sales growth alongside double-digit earnings-per-share growth.

Fourth, Berkshire made a brand new $350 million portfolio addition by purchasing shares of the New York Times Company. This is a classic Buffett legacy play. The nearly 175-year-old journalism institution has successfully transitioned from print to a digital-first model. They now boast over 12 million digital subscribers and have seen their digital advertising revenue soar. It is a highly influential, reliable media ecosystem that offers a safe place to park capital, even if its valuation commands a steep premium.

+2

Finally, Buffett added a small $40,000 top up to Lamar Advertising, a position he initially started last year with a $150 million purchase. Lamar is a real estate investment trust that controls over 360,000 physical billboards across North America. While digital advertising dominates the modern narrative, physical billboards are highly resilient assets that allow Lamar to pay a highly attractive 5 per cent dividend yield.

The Cash Fortress

When you combine the aggressive selling of tech giants with the highly selective buying of defensive legacy assets, you arrive at the most astonishing metric in modern finance. Berkshire Hathaway is sitting on hundreds of billions of dollars in cash and short-term treasury bills.

This figure is almost impossible to comprehend. It is more cash than the gross domestic product of many countries. Most importantly, it is vastly larger than the $44 billion cash pile Buffett held in 2007 just prior to the devastating global financial crisis. Back then, critics called him overly conservative and out of touch. When the markets collapsed, Buffett used that liquidity to bail out Goldman Sachs, buy railroads, and secure some of the most lucrative deals of his career.

Today, Buffett is explicitly stating that there is nothing attractive to buy at current valuations. He believes the stock market is simply too expensive and the risk-to-reward ratio is fundamentally broken. He is perfectly content earning a 5 per cent yield on government treasury bills rather than risking his capital in what he perceives as a massive bubble.

But this cash pile is not just a sign of patience. It is a terrifying macro warning. At the 2024 annual meeting, Buffett explicitly stated that the United States fiscal situation is entirely unsustainable. He told his shareholders that Berkshire must be positioned to survive scenarios that have literally never occurred before. This implies he is preparing for an unprecedented sovereign debt crisis, a collapse in dollar confidence, or a global monetary reset.

The Stealth $100 Billion Commodity Megabet

If the cash pile is Buffett’s shield, his hidden commodity portfolio is his sword. Over the last four years, the greatest stock picker in history has quietly executed the largest continuous commodity investment the financial world has ever seen.

The strategy began in 2020 when Buffett shocked Wall Street by purchasing shares in five mundane Japanese trading companies: Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo. Wall Street largely ignored the move, but these five companies are the undisputed titans of global resources. They control massive, diversified platforms that touch every critical commodity on earth, from copper and iron ore to natural gas and rare earth metals. Berkshire has continually added to these positions, turning the initial investment into a staggering $40 billion holding.

When you combine this Japanese trading block with Berkshire’s $30 billion stake in Occidental Petroleum, its massive Chevron holdings, the BNSF commodity railway network, and Berkshire Hathaway Energy, the total exposure to hard resources exceeds $100 billion.

Deep financial analysis suggests this is not merely an inflation hedge, but a highly calculated geopolitical manoeuvre regarding China. Buffett famously despised gold for decades, calling it an unproductive pet rock. Yet, in 2020, he briefly bought into Barrick Gold, the world’s second-largest gold miner. Some analysts believe this was a strategic intelligence gathering operation. It allowed Buffett to access internal board-level data on global central bank gold purchasing patterns.

This intelligence directly translates to his Japanese trading house investments. These five Japanese firms are the primary suppliers of raw materials to the Chinese market. They handle purchase orders, shipping volumes, and delivery logistics. By owning major stakes in these companies, Buffett has unparalleled, real-time visibility into China’s massive structural shift.

The data passing through these Japanese firms indicates that China is not just buying commodities for normal industrial use. They are actively engaged in historic, strategic stockpiling. Furthermore, China is increasingly settling these resource purchases in yuan rather than the US dollar. They are securing long-term supply contracts that permanently remove future commodity inventory from the global market. If China is indeed secretly accumulating massive gold reserves and hoarding base metals, a global supply shock is inevitable.

Buffett understands that when the world’s largest buyer accelerates demand while simultaneously choking off future global supply, prices will violently reprice upward.

The End of the Illusion

The mainstream financial media continues to cover Warren Buffett as if he is just tweaking a standard equity portfolio. They debate his slight reduction in Apple or his new pizza stock. But they are missing the forest for the trees.

The Oracle of Omaha has spent the past 4 years executing a comprehensive portfolio transformation. He is actively abandoning the offensive playbook that dominated the last decade of quantitative easing and zero-interest-rate policy. He is no longer playing the tech growth game. Instead, he has constructed an impenetrable defensive fortress designed to survive a massive fiscal crisis.

By hoarding cash, dumping financial sector stocks, and quietly amassing $100 billion in hard global commodities, Buffett’s money is screaming a warning that his public relations team cannot legally say out loud. He anticipates a devastating repricing of financial assets and a massive transfer of wealth toward tangible, physical resources.

Buffett has seen every financial panic, war, and market bubble over the last seventy years. He has never held this much cash or placed a commodity bet of this magnitude. As he steps away from the daily operations of his empire, his final masterstroke is complete. The greatest investor in human history has placed his chips on the table, and he is betting that the global financial system is about to break.

If you found value in this article, please hold down the like ❤️ button or consider buying me a coffee ☕️ to fuel the next one!